Insider Monkey

Insider Monkey |

- Christian Leone, Luxor Capital Increase Exposure in Hemisphere Media Group

- RCS Capital Reveals 8.3% Stake in Investors Capital Holdings

- Did Social Media Buzz Predict Carl Icahn’s Biggest Trades?

- 3 Billionaire Buys You Should Know About

- FS Capital Partners Reports Holding 43.5% of HHGregg

- Burgundy Asset Management Ups Positions in CBIZ and Ritchie Bros. Auctioneers

- Clinton Group Demands Shareholder Meeting at ValueVision

- Joseph Edelman’s Perceptive Advisors Buys More AcelRx Pharmaceuticals

- Heartland Advisors Discloses Changes in its Albany International and Gulf Island Holdings

- Bill Ackman Cuts Stake in LSE-listed Platform Specialty Products

- Chuck Royce Discloses Moves in Vera Bradley, Graham Corp & Others

- Opus Boosts Stake in Landec Corporation to Over 9%

- The 6 Most Dangerous Roads You Could Ever Drive On

- The 9 Weirdest Jobs in the World

- Do Your Mining Stocks Have The ‘Death Gene’?

- This Beaten-Down Retailer is Poised for 50% Gains in 2014

- Arguments For When The Fed Will Taper

- Kellogg Earnings Analysis: Understatement of Reported Net Income?

- Supercharge Your Portfolio With 2 Small-Cap Investments

- Profit From The Big Apple With This Real Estate IPO

| Christian Leone, Luxor Capital Increase Exposure in Hemisphere Media Group Posted: 06 Nov 2013 02:27 PM PST Christian Leone‘s fund, Luxor Capital Group, just upped its position in Hemisphere Media Group Inc (NASDAQ:HMTV) to 4.55 million shares, from some 2.34 million disclosed in its latest 13F. Luxor now holds 37.7% of Hemisphere’s common stock. Disclosure: none   | ||||||||||||||||||||||||||||||||||||||||||||||||

| RCS Capital Reveals 8.3% Stake in Investors Capital Holdings Posted: 06 Nov 2013 02:01 PM PST RCS Capital disclosed, in a new filing with the SEC, holding an activist stake in Investors Capital Holdings Ltd (NYSEMKT:ICH). The position amasses 598,258 shares, and represents 8.3% of Investors Capital’s common stock. Disclosure: none Recommended Reading: Did Social Media Buzz Predict Carl Icahn's Biggest Trades? 3 Billionaire Buys You Should Know About FS Capital Partners Reports Holding 43.5% of HHGregg | ||||||||||||||||||||||||||||||||||||||||||||||||

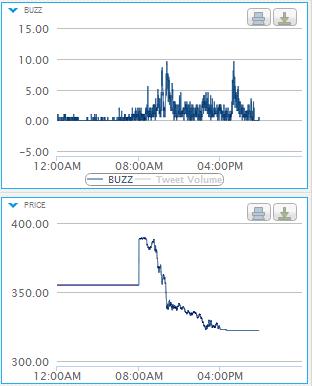

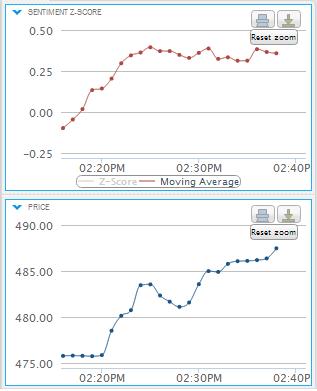

| Did Social Media Buzz Predict Carl Icahn’s Biggest Trades? Posted: 06 Nov 2013 01:50 PM PST There are a select few money managers whose words can move entire markets, but up to this point, only one has mastered the medium of Twitter Inc (NYSE:TWTR): Carl Icahn. After creating an account earlier this year, the billionaire has disclosed a few big positions on the micro blogging site, including a purchase of Apple Inc. (NASDAQ:AAPL) and a sale of Netflix, Inc. (NASDAQ:NFLX) stock. While the media has had a lot to say about Icahn's Twitter account, no one has taken the time to examine his trades in terms of social media sentiment. For someone who is likely the world's most socially active hedge fund manager, surprisingly little analysis has been done in this realm. With the help of Market Prophit, a company that converts stock-related social media posts into easy-to-read data, we're able to look at how much chatter Icahn's biggest trades created. More interestingly, it appears that some of this buzz actually predicted the moves before they happened. Netflix Netflix was the recipient of a major cut by Icahn late last month. In a 13D filing and subsequent tweet after the market's close on October 22nd, the investor reported a 4.5% stake in the streaming video company, about half of what he previously owned. This move came 24 hours after Netflix's stock price had surged on promising third quarter earnings. Market Prophit's CEO, Igor Gonta, revealed to us that on the morning of the 22nd, social media circles were already buzzing about a major seller "doing large block sales" of Netflix, and Icahn's name was visibly in the rumor mill. By the time the market had closed, Icahn's official SEC disclosure pressed the stock to drop almost all of its gains from the previous day's earnings report. Apple Any analysis of Carl Icahn and Twitter must include Apple. On the afternoon of August 13th this year, Icahn tweeted that he had a "large position" in the tech giant on the basis of undervaluation, adding that a conversation with Tim Cook was on the table. As Gonta pointed out to us, shares of Apple rallied by nearly 2.5% just 20 minutes after Icahn's initial tweet, and social media sentiment turned positive approximately two minutes prior to the reveal (see graph here). The next major event on the Icahn-Apple timeline was on October 1st. Halfway through the morning on this date, Icahn tweeted about the dinner he had with Tim Cook the night before, in which he reiterated his desire for Apple to pursue a $150 billion share buyback plan. Market Prophit again picked up on bullish chatter before Icahn's tweet went live at 10:23am. This time, an uptick in positive social chatter led the tweet by a full 40 minutes, and shares of Apple had already risen by almost one full percentage point by half past ten. According to Gonta, social media sentiment turned negative immediately following Icahn's tweet "because the price had already run up," indicating that a classic "sell the news" phenomenon had just taken place. Sitting here in early November, it's unknown if Icahn will succeed in his quest to convince Apple that a larger buyback will lead to a $1,250 stock price. What we can say with confidence, though, is if the hedge fund manager is active on Twitter again, social media chatter may predict it. Disclosure: none Recommended Reading: 3 Billionaire Buys You Should Know About Clinton Group Demands Shareholder Meeting at ValueVision Hedge Fund News: Dan Loeb, George Soros & Seth Klarman | ||||||||||||||||||||||||||||||||||||||||||||||||

| 3 Billionaire Buys You Should Know About Posted: 06 Nov 2013 01:01 PM PST There are dozens of hedge fund transactions on a daily basis, but only a few billionaires change their positions each week. You're probably aware of high net-worth guys like Warren Buffett and George Soros, but there are some other billionaires buys you should know about. Because it's important to track the smart money's best and brightest (discover how investors have beaten the market with this strategy), let's take a look at three in particular from the past week. Bill Gates and KiOR KiOR Inc (NASDAQ:KIOR), the small-cap renewable fuels development company, doesn't have much interest from the prominent investors we track. According to a new SEC filing from Bill Gates and Gates Ventures, though, the co-founder of Microsoft Corporation (NASDAQ:MSFT) now owns 11.8% of Kior's outstanding stock. The total position is about 7.4 million shares worth $16.8 million at current market prices; only Stuart Peterson's Artis Capital appears to be a bigger bull. Of course, there are many reasons why Gates could be interested in Kior, but as one corporate PR statement shows, it's probably due to the actual mission of the company itself. Gates publicly stated that he "was impressed" with Kior's commercial scale cellulosic fuel facility in Columbus, Mississippi, adding that he's looking to "move its technology forward." For any wealthy investor looking to put his or her money behind an environmental cause and not just an investment, Kior provides that opportunity. The company's is working on a novel proprietary technique that converts non-food biomass into fuels ready to be used by existing automobiles. Wall Street doesn't expect Kior to be profitable for at least a few years (it expects an EPS of $-1.30 this year and $-0.88 in 2014), but it isn't particularly expensive at 2.3 times its book value. Free cash flows are negative, but have improved significantly since 2011, and Kior's debt is manageable. Credit Suisse, one of the few agencies that covers Kior, holds an outperform rating on the stock. According to Credit Suisse analyst Edward Westlake, the basis for this bullishness lies in the assumption that by 2015, "KiOR would be cash flow positive as a corporation and significantly better positioned to pursue the longer-term growth of turning non-food wood or waste products into fuel." If you are invested here, keep this general timeline in the back of your mind, and be on the lookout for any Kior news that could accelerate or slow Westlake's outlook. It is one of the main ideas driving the stock's growth estimates—Wall Street as a whole expects Kior to generate EPS growth 34% a year over the next half-decade. It's worth noting that Bill Gates' stake here is passive in nature; don't expect any activist influence from the billionaire. Howard Marks and Contango In a 13D filing at the end of last month, Howard Marks and Oaktree Capital Management disclosed a 6.8% activist stake in Contango Oil & Gas Company (NYSEMKT:MCF). The position amasses 1.3 million shares worth a total of $55.3 million. Ric Dillon, Chuck Royce and Ken Griffin are also invested in the natural gas and oil company, and Marks' buy comes amid Oaktree's closure of its entire position in Crimson Exploration Inc. (NASDAQ:CXPO). Both energy players closed their merger in early October, and the newly combined company will maintain its offshore operations in the Gulf with additional onshore production in Texas. From a macroeconomic standpoint, it's easy to see why Marks continues to be bullish post-merger. The domestic E&P industry is currently in the midst of a solid uptrend, particularly in oil and liquids versus lesser growth in natural gas, and Contango's purchase of Crimson gives it healthier diversification in both of these areas. On average, the sell-side estimates there's about an 18% upside to Contango shares presently, so if you're a fan of Marks and Oaktree, it'd be smart to take a longer look here. Tiger Global and Carter's Tiger Global is a massive hedge fund managed by billionaire Chase Coleman and Feroz Dewan, and the legendary Julian Robertson seeded it. In a passive SEC filing on October 31st, Tiger Global reported that it upped its stake in Carter’s, Inc. (NYSE:CRI) to 5.65 million shares, versus 4 million held in its last 13F. The newly increased position now represents 10.4% of the young children's apparel marketer, which has seen its shares rise by 25.8% year-to-date. The Tiger cub's boost in Carter's comes at an interesting time, when shares already trade at fair valuation multiples and are oversold according to some analysts. As Coleman and Dewan often do, though, we believe they are invested in Carter's due to its growth prospects. The company has beaten Wall Street's earnings estimates in every quarter of 2013, which are the same estimates that forecast annual EPS growth of 17% through 2018. In May of this year, Carter's announced its first-ever quarterly dividend, which amounts to a yield of just below 1%, and its meager payout ratio near 5% indicates there's more upside for income-seeking investors. The company's ability to both sell and license its product lines, which include Carter's, Child of Mine, Just One Year, Precious Firsts, and yes, Oshkosh, is an added strength that Tiger Global is likely bullish on. In general, this attribute should provide more stability to Carter's future growth prospects. Disclosure: none Recommended Reading: FS Capital Partners Reports Holding 43.5% of HHGregg Clinton Group Demands Shareholder Meeting at ValueVision Heartland Advisors Discloses Changes in its Albany International and Gulf Island Holdings | ||||||||||||||||||||||||||||||||||||||||||||||||

| FS Capital Partners Reports Holding 43.5% of HHGregg Posted: 06 Nov 2013 11:53 AM PST In a newly amended filing, FS Capital Partners disclosed holding around 13.5 million shares of hhgregg, Inc. (NYSE:HGG). The position amasses 43.5% of the company’s common stock. Disclosure: none Recommended Reading: Burgundy Asset Management Ups Positions in CBIZ and Ritchie Bros. Auctioneers Joseph Edelman's Perceptive Advisors Buys More AcelRx Pharmaceuticals Heartland Advisors Discloses Changes in its Albany International and Gulf Island Holdings | ||||||||||||||||||||||||||||||||||||||||||||||||

| Burgundy Asset Management Ups Positions in CBIZ and Ritchie Bros. Auctioneers Posted: 06 Nov 2013 11:50 AM PST In two new filings, Burgundy Asset Management disclosed changes it applied to positions in CBIZ, Inc. (NYSE:CBZ) and Ritchie Bros. Auctioneers (USA) (NYSE:RBA). In CBIZ, Burgundy upped its holding to almost 4.99 million shares, from slightly above 1.0 million disclosed in its latest 13F. The position represents 10.58% of the company’s common stock. In Ritchie Bros., Burgundy now holds around 11.39 million shares, equal to 10.66% of the company. This is an increase from the 9.2 million shares owned earlier. Disclosure: none Recommended Reading: Clinton Group Demands Shareholder Meeting at ValueVision Joseph Edelman's Perceptive Advisors Buys More AcelRx Pharmaceuticals Heartland Advisors Discloses Changes in its Albany International and Gulf Island Holdings | ||||||||||||||||||||||||||||||||||||||||||||||||

| Clinton Group Demands Shareholder Meeting at ValueVision Posted: 06 Nov 2013 11:33 AM PST Clinton Group, in a newly amended filing, disclosed a letter, sent to Keith R. Stewart, Chief Executive Officer of ValueVision Media Inc (NASDAQ:VVTV), in which it demanded a special meeting of shareholders of the company. Clinton demands several points to be discussed during the meeting, including changes to ValueVision’s Board. Check out the letter sent by Clinton to Keith R. Stewart below: Clinton Group Letter to ValueVision Earlier this week, Clinton disclosed forming an activist group with Carlo Cannell and his hedge fund Cannell Capital at ValueVision. Disclosure: none Recommended Reading: Joseph Edelman's Perceptive Advisors Buys More AcelRx Pharmaceuticals Heartland Advisors Discloses Changes in its Albany International and Gulf Island Holdings Bill Ackman Cuts Stake in LSE-listed Platform Specialty Products | ||||||||||||||||||||||||||||||||||||||||||||||||

| Joseph Edelman’s Perceptive Advisors Buys More AcelRx Pharmaceuticals Posted: 06 Nov 2013 10:58 AM PST Joseph Edelman‘s fund, Perceptive Advisors, in a new filing reported increasing its position in AcelRx Pharmaceuticals Inc (NASDAQ:ACRX) again, after disclosing a buy of around 360,700 shares a couple of days ago. This time, Perceptive acquired 155,000 shares, bringing the position to a total of some 6.37 million shares. The average purchase price amounts to around $6.87 per share. Disclosure: none Recommended Reading: Heartland Advisors Discloses Changes in its Albany International and Gulf Island Holdings Bill Ackman Cuts Stake in LSE-listed Platform Specialty Products Chuck Royce Discloses Moves in Vera Bradley, Graham Corp & Others | ||||||||||||||||||||||||||||||||||||||||||||||||

| Heartland Advisors Discloses Changes in its Albany International and Gulf Island Holdings Posted: 06 Nov 2013 09:33 AM PST Heartland Advisors, in two new filings, disclosed changes in its holdings in Albany International Corp. (NYSE:AIN) and Gulf Island Fabrication, Inc. (NASDAQ:GIFI). The fund reported holding 1,326,631 shares of Albany International, which represent 4.7% of the company’s common stock. The stake has declined from 1,838,773 shares reported in the latest 13F. In Gulf Island, Heartland disclosed a 10% stake, which amasses 1,453,992 shares, slightly up from 1,413,195 shares held at the end of the second quarter. Disclosure: none Recommended Reading: Bill Ackman Cuts Stake in LSE-listed Platform Specialty Products Chuck Royce Discloses Moves in Vera Bradley, Graham Corp & Others Opus Boosts Stake in Landec Corporation to Over 9% | ||||||||||||||||||||||||||||||||||||||||||||||||

| Bill Ackman Cuts Stake in LSE-listed Platform Specialty Products Posted: 06 Nov 2013 08:57 AM PST Bill Ackman‘s hedge fund, Pershing Square, has just disclosed it is decreasing its position in Platform Specialty Products Corp (LON:PAH). Pershing now owns over 66.4 million in voting rights of the company, which represent 64.88% of the class, down from 75.07% held earlier. The stake involves around 28.96 million shares held directly, 29.17 million voting rights owned indirectly, and more than 8.3 million voting rights in the form of warrants to exchange for ordinary shares. Disclosure: none Recommended Reading: Chuck Royce Discloses Moves in Vera Bradley, Graham Corp & Others Stadium Capital Unloads Shares of Big 5 Sporting Goods Red Oak Cuts Stake in Digirad Corporation to 2.8% | ||||||||||||||||||||||||||||||||||||||||||||||||

| Chuck Royce Discloses Moves in Vera Bradley, Graham Corp & Others Posted: 06 Nov 2013 08:38 AM PST Chuck Royce‘s Royce & Associates continues reporting moves in several companies. After yesterday’s disclosure that it was altering six of its holdings, today, the fund filed three more 13Gs with the Securities and Exchange Commission. The stocks involved were Vera Bradley, Inc. (NASDAQ:VRA), Graham Corporation (NYSEMKT:GHM), Ampco-Pittsburgh Corp (NYSE:AP), and Lincoln Electric Holdings, Inc. (NASDAQ:LECO). In Vera Bradley, Royce now holds 4.44 million shares, up from 3.17 million mentioned in its latest 13F. Following the increase, Royce’s position now amasses 10.94% of company’s common stock. Royce also disclosed reducing its exposure in Graham Corporation to 585,385 shares, which are equal to 5.82% of the common stock. The position held by Royce earlier involved 765,785 shares of Graham. In Ampco-Pittsburgh, Royce reported holding a 7.62% stake, which amasses 789,547 shares, down from some 1.4 million held previously. The fourth filing disclosed Royce holding 4.3 million shares of Lincoln Electric, equal to 5.25% of the common stock. The position has been cut from around 7.02 million shares reported in the latest 13F. Disclosure: none Recommended Reading: Opus Boosts Stake in Landec Corporation to Over 9% Hedge Fund News: Dan Loeb, George Soros & Seth Klarman Clinton Group Lowers Activist Stake in NutriSystem | ||||||||||||||||||||||||||||||||||||||||||||||||

| Opus Boosts Stake in Landec Corporation to Over 9% Posted: 06 Nov 2013 07:37 AM PST Opus Capital Group, in a newly amended filing with the SEC, disclosed boosting its passive stake in Landec Corporation (NASDAQ:LNDC) to some 2.55 million shares, from around 1.83 million shares reported in an earlier filing. The increased stake now amasses 9.62% of the company’s common stock. Disclosure: none Recommended Reading: Hedge Fund News: Dan Loeb, George Soros & Seth Klarman Clinton Group Lowers Activist Stake in NutriSystem Stadium Capital Unloads Shares of Big 5 Sporting Goods | ||||||||||||||||||||||||||||||||||||||||||||||||

| The 6 Most Dangerous Roads You Could Ever Drive On Posted: 06 Nov 2013 07:15 AM PST Most dangerous roads: Do you know which are the most dangerous roads in the world? Regardless of how experienced a driver you are, some roads tend to be harder to tackle than others. We have compiled a list of the 6 most dangerous roads in the world, in a style similar to our coverage of the most dangerous jobs. After reading the countdown, you'll be glad that the only thing you have to worry about each day on your way to work is a traffic jam. Let's take a look at the most dangerous roads: | ||||||||||||||||||||||||||||||||||||||||||||||||

| The 9 Weirdest Jobs in the World Posted: 06 Nov 2013 07:07 AM PST Weirdest jobs: While it is true that we can't all be doctors, lawyers, or accountants, some people out there have some of the most odd and peculiar jobs. But what makes someone choose a strange career path? In some cases, it may be the profit. For others, is the fact that they have a unique talent to offer. We would like to present you with a list of the most peculiar jobs in the world, in a style similar to our coverage of the best summer jobs for students. They couldn’t be more opposite. Want to know what else is unique about these jobs apart from their line of work? Most of them are actually paid very well. Let's take a look at the 9 weirdest jobs we could find: | ||||||||||||||||||||||||||||||||||||||||||||||||

| Do Your Mining Stocks Have The ‘Death Gene’? Posted: 06 Nov 2013 07:02 AM PST

Not to worry — I’ll tell you about an antidote in a moment, but first consider this… The death gene is the genetic variant that apparently can determine — with disconcerting accuracy — your likely departure time from this planet. Researchers in Boston inadvertently made the discovery in the aftermath of a study that looked at sleep patterns. The scientists found that subjects with one particular genetic arrangement died just before 11 a.m., while another group with a different makeup passed away around 6 p.m. Dave Forest, Chief Investment Strategist for StreetAuthority’s Junior Resource Advisor, recently discovered a new kind of death gene. It may not predict the demise to the hour like the Boston findings do, but it does tell us to the year — and even the month — when some of the biggest companies in the market might suddenly implode, and perhaps even cease to exist. This potential terminal switch is something investors have grown so accustomed to that few think of it as a problem. But I believe it’s going to rear its ugly head soon and perhaps often — destroying billions in shareholder value, as formerly vibrant businesses are swiftly and suddenly rendered paralytic and inoperable. In this instance, the Grim Reaper is debt. The thing about debt, of course, is that sooner or later it comes due. And if a company doesn’t have the cash to pay back maturing obligations or the ability to otherwise extend or “roll” the debt, the maturity date “is also the time when debt can turn into a death gene, wreaking havoc on firms that may appear to be healthy,” Dave writes. Dave pays particular attention to natural resource companies, a sector in which many of the big players — along with some of the smaller ones — are going to be facing potentially challenging payback issues over the next few years. That’s because falling commodity prices are squeezing cash flow and impeding the ability of borrowers to service or pay off their debts, according to Dave. Integrated miners BHP Billiton Limited (ADR) (NYSE:BHP) and Vale SA (ADR) (NYSE:VALE), along with gold major Barrick Gold Corporation (USA) (NYSE:ABX), for instance, have large debt obligations that mature in 2013. These obligations equal nearly half of the annualized cash generated by the operations of these companies. And for BHP and Barrick, it doesn’t end there: Each has some fairly significant debt-rolling to manage in 2014 and 2015. If investors won’t roll the debt, these particular companies likely will be able to cover their loans from cash flow. But extinguishing the debt in this manner would take a significant bite out of available cash. Advantage: junior resource firms — companies that most investors haven’t yet discovered. The types of companies that have the potential to soar as their businesses grow. The types of companies that have little or no debt. The types of companies Dave writes about each month in Junior Resource Advisor. And therein lies the antidote to the death gene… Bob: How does debt factor in to your stock selection process in Junior Resource Advisor? What’s the advantage of your methodology? | ||||||||||||||||||||||||||||||||||||||||||||||||

| This Beaten-Down Retailer is Poised for 50% Gains in 2014 Posted: 06 Nov 2013 07:01 AM PST

Few appear to have been as hard hit as women’s apparel and accessory retailer Francesca’s Holdings Corp (NASDAQ:FRAN). In early September, Francesca’s announced that same-store sales, which had been growing at a fast pace ever since its July 2011 IPO, had suddenly turned negative. Investors were in an unforgiving mood, and shares fell sharply to a 52-week low. News of the sudden sales slowdown led many to question if this once-hot retailer was still capable of robust growth. Sales had risen 45% in fiscal 2013 to nearly $300 million, leading to a 100% spike in 2013 earnings per share (EPS). Though analysts had been expecting another banner year in fiscal 2014, they now expect FRAN to boost sales only 17% (based entirely on new store openings) and grow EPS less than 10%. Yet investors shouldn’t conclude that FRAN’s business model is broken. Instead, the recent slowdown can be chalked up to growing pains. And with sales growth expected to re-accelerate in fiscal 2015 to around 20%, investors will again start focusing on this retailer’s very impressive operating metrics. To be sure, FRAN’s management concedes the in-store merchandise wasn’t especially compelling in recent months — quite a turnabout for a company known for a deft merchandising touch. On the quarterly conference call, management explained, “There has not been a dominant fashion trend to drive and chase in apparel category this season.” Management also noted that FRAN’s long lead times led the retailer to miss out on any fashion themes that did emerge this summer. Also, the company said that gift items, which account for roughly 10% of sales, were poorly selected by the company’s merchandisers. “We recognize the assortment needs to be refined,” said CEO Neill Davis on the conference call. To be sure, investors don’t expect stellar results for the current quarter, ended in October, nor should they expect solid upside from the holiday season. But as the next fiscal year gets under way in February, FRAN looks set to exceed a low set of expectations. For example, the company is on track to open roughly 80 stores in the current fiscal year, expanding the store base by around 20% to over 450 stores. That’s roughly in line with the projected sales growth rate for next year, implying that same-store sales will be flat. Yet that view is likely too pessimistic. After all, the company posted a slight 1% drop in sales in the most recent quarter, as a 4% drop in traffic was mostly offset by a 3% increase in average transaction prices. Assuming traffic stabilizes in the coming fiscal year and those 3% price increases stick, you already have a recipe for modest same-store sales growth. Management expects same-store sales growth to be better than modest. “As we step into the spring of 2014, I feel very good about what the merch[andise] is going to be able to bring to the table and the responsiveness of our customers,” noted Davis. | ||||||||||||||||||||||||||||||||||||||||||||||||

| Arguments For When The Fed Will Taper Posted: 06 Nov 2013 06:13 AM PST The general consensus is that the U.S. Federal Reserve will not begin to taper its asset purchases until sometime in 2014. Economic growth remains flaccid, and the federal government shutdown certainly didn't help the situation. Deutsche Bank makes the arguments the Fed will be considering when deciding whether to taper in December or wait until March. A slow labor market is what has many analysts opting on the side of no taper until next year. Floating Path explores economic and cultural phenomena, and hopes to educate, inspire and provoke. Discover their wide range of daily content here. | ||||||||||||||||||||||||||||||||||||||||||||||||

| Kellogg Earnings Analysis: Understatement of Reported Net Income? Posted: 06 Nov 2013 06:13 AM PST Kellogg Earnings AnalysisYesterday, Kellogg Company (NYSE:K) reported preliminary financial results for the quarter ended 2013-09-30 (full transcript). Stocks in the food processing industry have seen an overall increase of over 35%this year while Kellogg stock has only seen a year-to-date change of over 12%. Kellogg operates as a food manufacturing company. Its brands include Kellogg’s, Keebler, Pop-Tarts, Eggo, Cheez-It, Nutri-Grain, Rice Krispies, Murray, Austin, Morningstar Farms, Famous Amos, Carr’s, Plantation, Ready Crust and Kashi, which are manufactured in 18 countries and marketed in more than 180 countries. Our peer-based analysis of Kellogg Company (peer set at the end of the post) looks at the company’s performance over the last twelve months (unless stated otherwise). The table below shows the preliminary results along with the recent trend for revenues, net income and returns.

Valuation DriversKellogg Company’s current Price/Book of 8.0 is about average in its peer group. Kellogg’s operating performance is higher than the average of its chosen peers (ROE of 36.3% compared to the peer average ROE of 23.8%) but the market does not seem to expect higher growth relative to peers (PE of 23.9 compared to peer average of 23.9) but simply to maintain its relatively high rates of return. The company’s asset efficiency (asset turns of 1.0x) and net profit margins of 6.4% are both average for its peer group. Kellogg’s net margin is its lowest relative to the last five years and compares to a high of 10.1% in 2010. Long-term strategic betWhile Kellogg’s revenues growth has been below the peer average in the last few years (4.1% vs. 6.3% respectively for the past three years), the market still gives the stock an about peer average PE ratio of 23.9. The market seems to see the company as a long-term strategic bet. Kellogg’s annualized rate of change in capital of 13.0% over the past three years is around its peer average of 15.3%. This average investment has likewise generated a peer average return on capital of 14.2% averaged over the same three years. This average return on investment implies that company is investing appropriately. Kellogg Earnings Quality– Possible Understatement of Net Income?Kellogg’s net income margin for the last twelve months is around the peer average (6.4% vs. peer average of 6.6%). This average margin and relatively conservative accrual policy (5.5% vs. peer average of 4.2%) suggests possible understatement of its reported net income. Kellogg’s accruals over the last twelve months are positive suggesting a buildup of reserves. In addition, the level of accrual is greater than the peer average — which suggests a relatively strong buildup in reserves compared to its peers. Trend Charts for Kellogg Company (NYSE:K)Peers used for Kellogg Earnings AnalysisKellogg Earnings Analysis used the following peer-set: PepsiCo, Inc. (NYSE:PEP), Mondelez International Inc (NASDAQ:MDLZ), General Mills, Inc. (NYSE:GIS), Flowers Foods, Inc. (NYSE:FLO), The Hain Celestial Group, Inc. (NASDAQ:HAIN) and TreeHouse Foods Inc. (NYSE:THS). | ||||||||||||||||||||||||||||||||||||||||||||||||

| Supercharge Your Portfolio With 2 Small-Cap Investments Posted: 06 Nov 2013 06:12 AM PST

You get the same power when you take two high-flying sectors of the market and combine them into a single exchange-traded fund (ETF). That is the true beauty behind ETFs: the ability to invest in very precise niches of the market that, when multiplied, result in head-turning returns. Today, let’s look at a combination of small caps with health care and technology. Small-caps stocks have been on a tear and are poised to continue their streak for some time longer. The iShares S&P SmallCap 600 Index (ETF) (NYSEARCA:IJR) hit an all-time high Oct. 29 and is up about 28% year to date. In fact, this index of core small caps is up 36% over the past 12 months, 50% over the past two years and 130% over the past five, outpacing the Dow Jones Industrial Average on all fronts. As Bloomberg reports, in three out of the past four periods in which small-caps trounced the Dow so dramatically, equities kept moving higher and the U.S. economy strengthened the following year. Investing in individual small-cap stocks can be tricky, though. They’re capable of running up the hill very quickly but going downhill twice as fast — with a steeper drop. That’s why I love these two ETFs: PowerShares S&P SmallCap Hlth Cr Ptflo (NASDAQ:PSCH) and PowerShares S&P SmlCp Inftn Thgy Pfo (NASDAQ:PSCT). Up 38% and 33% year to date, respectively, these two top-performing ETFs offer safer ways to capitalize. Let’s take a look at each ETF. PowerShares S&P SmallCap Hlth Cr Ptflo This ETF benefits directly from the trends of the “Graying of America,” higher medical costs, the Affordable Care Act (aka Obamacare), etc. The 65 companies that make up the ETF obviously do business in health care products and services, but that includes a nice mix of pharmaceuticals, medical technology and supplies, and biotechnology. While 72.9% of the fund is composed of small-cap growth companies and another 16.5% is small-cap value stocks, it includes a 10.6% stake in mid-cap growth as well. Its top holdings include: Centene Corp (NYSE:CNC), a company involved in Medicare and Medicaid programs and services. Its revenue from services for the third quarter totaled $2.7 billion, a 24% increase from the same period last year. CNC is up 35% year to date. Align Technology, Inc. (NASDAQ:ALGN), maker of invisible dental braces, reported a 62% increase in third-quarter revenue over 2012. ALGN is up nearly 100% in 2013. Questcor Pharmaceuticals Inc (NASDAQ:QCOR), maker of drugs for the treatment of multiple sclerosis, has been popular as of late, with an average 1.1 million shares trading over 30 days. No surprise why: QCOR is up 109% year to date. With average trading volume around 28,000 shares a day and $156 million in assets, PSCH is a thinly traded ETF with plenty of potential. PowerShares S&P SmlCp Inftn Thgy Pfo Small caps and information technology (IT) stocks are a match made in heaven. IT is perhaps the largest growing market domestically and internationally with plenty of smaller companies positioned to take their share of it. | ||||||||||||||||||||||||||||||||||||||||||||||||

| Profit From The Big Apple With This Real Estate IPO Posted: 06 Nov 2013 06:12 AM PST

The tiny, 34-square-mile island is home to Wall Street, the global headquarters of the United Nations and some of the most powerful and influential companies in the world. That exclusivity has driven big gains for one of Manhattan’s most prized properties. Since going public in the spring of 2010, The Madison Square Garden Co (NASDAQ:MSG) is up a market-crushing 198%. But if you missed out on that impressive run, don’t worry. The most exclusive real estate market in the world is setting the stage for another big winner. Clocking in at $1.3 billion, this company’s recent IPO was the second-largest ever for a U.S. REIT (real-estate investment trust). It controls more than 8 million square feet of some of the most desirable commercial real estate in the world. And it also pays investors to own shares with a solid dividend yield that is higher than the benchmark 10-year Treasury. Empire State Realty Trust Inc (NYSE:ESRT) went public in early October. The REIT owns 12 office properties and six retail properties. The trust’s prized asset is the iconic Empire State Building, which is the second-tallest building in New York City. Not only is the Empire State Building one of the world’s most recognizable buildings, but it’s also located in one of New York’s strongest real estate markets, with the nation’s lowest local vacancy rates. A report from leading global real estate specialist CBRE shows Manhattan leasing rates are accelerating, with overall leasing activity in September rising 16% from last year and 36% from just last month while availability rates fell 20 basis points to 12.3%. Those macro tailwinds will continue to support leasing demand in the Empire State Building and the trust’s other properties in Manhattan. But the Empire State Building isn’t just an investment in commercial real estate. It’s also a play on one of the most popular tourist destinations New York City has to offer. The Empire State Building generates 40% of its revenue from selling tickets to its observation decks. That provides a nice source of revenue diversification against any short-term weakness in commercial real estate. Even though the Empire State Building is the flagship asset for Empire Realty Trust, one of the knocks against the building is its lease rate of 78%, well below some of its neighborhood peers trending between 94% and 96%. But that subpar lease rate is set to climb as the building continues to execute a $550 million investment project to upgrade infrastructure, tenant suites and lower energy costs. Lead contractor Johnson Controls, Inc. (NYSE:JCI) projects that the upgrade will cut the building’s energy consumption by 38% and save $4.4 million annually when finished and lease rates accelerate. That will continue to attract new tenants for the Empire State Building’s smaller office spaces that are in demand from the large number of media and technology startups operating in Manhattan. |

Have you heard about the “death gene”?

Have you heard about the “death gene”?

| You are subscribed to email updates from Insider Monkey - Free Hedge Fund and Insider Trading Data To stop receiving these emails, you may unsubscribe now. | Email delivery powered by Google |

| Google Inc., 20 West Kinzie, Chicago IL USA 60610 | |

Ditulis oleh Unknown

Rating Blog 5 dari 5

{kind=link}

{kind=link}

{kind=link}

0 komentar:

Posting Komentar